Home & Decor Blogs: DIY, Interior Design & Lifestyle Ideas

Why More Filipinos Are Using Credit Lines to Fund Home Improvements Instead of Loans

PHP 11,600 per square metre. That’s the average construction cost the Philippine Statistics Authority reported for June 2025, down about 3.1% from the same month a year earlier. Sounds almost affordable until you remember that’s the national average — including bare-bones projects in provinces where labour costs a fraction of what it does in Metro Manila. Build anything mid-range in Makati, Cebu, or Davao, and you’re looking at PHP 25,000 to PHP 35,000 per square metre. A modest 80-square-metre house at that rate is PHP 2 million before you’ve bought a single piece of furniture.

And that’s new construction. Renovations are a different headache entirely — one that Filipino homeowners deal with constantly. Roofs damaged by the typhoon season. Kitchens that haven’t been touched since the house was built. Bathrooms where the tile grout has gone from white to something you’d rather not examine too closely. The residential sector accounted for 68.6% of all approved building permits in June 2025, with single-type houses making up nearly 90% of those. People aren’t just building new. They’re fixing, expanding, and upgrading what they already have.

The question that keeps coming up is how to pay for it. And for a growing number of Filipinos, the answer isn’t a traditional bank loan anymore.

Loans Don’t Match How Renovations Work

A bank loan gives you a lump sum. If you borrow PHP 300,000, you start paying interest on PHP 300,000 from day one. That structure makes perfect sense for buying a property — one transaction, one price, done.

Renovations don’t work that way. You pay the contractor a down payment. Then the materials arrive, and you settle that bill. Then the electrician needs to come back because the wiring behind the wall was worse than expected. Then the tiles you ordered are out of stock, and the replacement costs more. Three weeks in, you’ve spent PHP 180,000 of your PHP 300,000 loan, but you’ve been paying interest on the full amount since you signed the paperwork.

Credit lines flip this. You have a borrowing limit — say, PHP 300,000 — and you draw from it as expenses come up. PHP 50,000 this week for materials. PHP 30,000 next week for labour. Interest only runs on what you’ve actually pulled out. When you repay a chunk, that capacity opens back up without filing a new application. For phased renovation spending where costs keep shifting, the difference in what you end up paying in interest is real.

What’s Happening With Rates

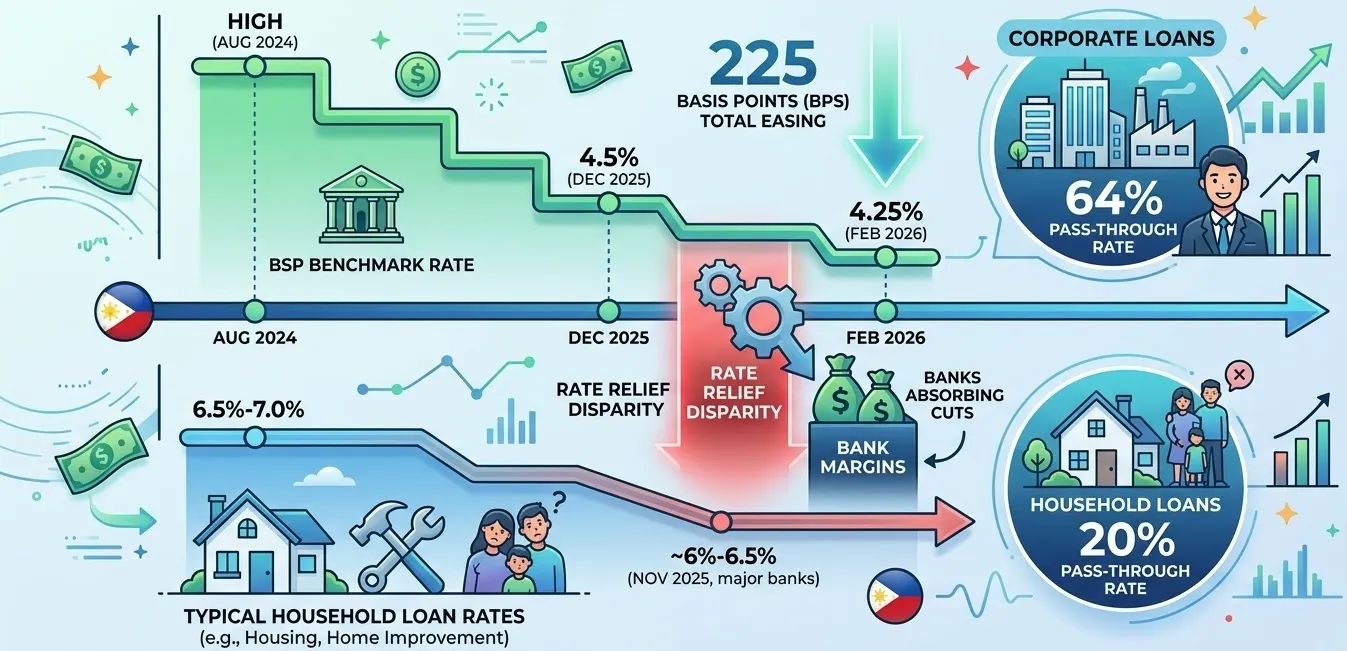

The BSP cut its benchmark rate five times through 2025, bringing it to 4.5% by December — the lowest since October 2022. Another cut in February 2026 dropped it to 4.25%, totalling 225 basis points of easing since August 2024.

Filipino borrowers haven’t felt much of that relief, though. Bloomberg reported in November 2025 that major banks like BDO were still charging around 6% to 6.5% on new housing loans, barely different from 2024. An AMRO analysis from March 2025 explained why: the pass-through rate from BSP policy changes to household lending rates was only about 20%. Corporate loans saw 64% pass-through. Household loans? A fifth. Banks were absorbing the cuts into their own margins rather than passing them to individual borrowers.

Home loan rates across Philippine banks currently sit between 6.25% and 10.5%, depending on the lender and how long you lock in. The longer the term, the higher the rate. For a 20-year mortgage, you’re at the expensive end. For shorter-term home improvement borrowing — the PHP 100,000 to PHP 500,000 range that most renovation projects fall into — credit lines often work out cheaper because you’re not carrying interest on unused money for months while your contractor takes their time finishing the job.

Freelancers Can’t Get Traditional Loans Easily

Upwork has consistently ranked the Philippines among its top freelancer countries. Grab drivers, online sellers, virtual assistants, content creators, food delivery riders — the gig workforce here is enormous. These people earn enough to own homes and improve them. What they often can’t produce is the stack of documents a bank wants before approving a loan: employment certificates, payslips from one employer, tax returns showing steady monthly income from a single source.

A freelance graphic designer earning PHP 60,000 a month across four clients is a perfectly creditworthy person. To a traditional bank’s loan approval system, they might as well be unemployed. The documentation requirements weren’t designed for how millions of Filipinos actually work now.

Digital credit lines have stepped into that gap. Approval leans on transaction history, repayment behaviour, and digital footprint rather than employment paperwork from a company’s HR department. For someone who needs PHP 150,000 to fix a roof before the next typhoon season hits and can repay across three months of project earnings, the accessibility matters enormously. A Salmon credit line is one option that’s gained users among Filipino borrowers specifically because the application process doesn’t punish you for being self-employed.

What Renovations Cost

Every Filipino homeowner who’s done a renovation has a story about how the budget went sideways. The numbers below are rough ranges — Metro Manila sits at the higher end, provincial areas lower, but they give you a realistic starting point.

| Project | Typical Range (PHP) |

|---|---|

| Kitchen renovation, mid-range | 150,000 – 400,000 |

| Bathroom retiling + new fixtures | 50,000 – 150,000 |

| Roof repair or full replacement | 80,000 – 300,000 |

| Room addition, basic (per sqm) | 15,000 – 25,000 |

| Whole-house electrical rewiring | 30,000 – 80,000 |

| Exterior repainting | 20,000 – 60,000 |

Material prices remain unpredictable. Typhoon-related supply disruptions hit construction materials hard during wet season — cement, steel, roofing — and prices spike when demand surges after storm damage across multiple provinces simultaneously. The PSA data showing a 3.1% year-over-year drop in average construction costs for June 2025 is encouraging, but that’s an average smoothed across the entire country. Individual project costs in your barangay will depend on what’s available at your local hardware supplier that month.

For projects in the PHP 50,000 to PHP 300,000 range — which covers most of the renovation work Filipino homeowners actually do — a credit line lets you start work when you need to, draw funds as contractor invoices come due, and stop paying interest the moment you repay. A fixed loan for the same amount forces you to guess your total cost upfront (almost always wrong) and start the interest clock on all of it whether you spend it this week or two months from now.

Not Burning the Credit Line

Credit flexibility is only useful if you don’t treat the available balance as money you already have. A few things that keep it manageable:

- Borrow for repairs that prevent bigger damage. Fixing a leaking roof before rainy season costs a fraction of repairing water damage to walls, ceilings, and electrical systems after four months of monsoon rain gets inside. That’s a sensible use of credit. Buying a new living room set because the limit was available is a different conversation.

- Filipino contractors typically work on progress billing — you pay a percentage at each milestone rather than everything upfront. Match your credit draws to those milestones. If the contractor asks for 30% down, 30% at rough-in, and 40% at completion, pull exactly those amounts at exactly those stages.

- Repay during strong months. Freelancer income in the Philippines often peaks in Q4 when international clients increase spending. If you’re renovating in Q3, plan the repayment schedule around Q4 cash flow. The revolving nature of a credit line means your repaid capacity is available again if something else comes up.

- And read the terms before signing anything. Interest rates, processing fees, late penalties, and how the revolving reset works — these vary between providers, and the differences compound over months of active borrowing. Five minutes of reading the fine print saves you from surprises that are much harder to fix later.

Where This Is Going

The Philippine construction industry is projected to reach $66.41 billion by 2031, growing at roughly 6.5% annually. Residential work remains the biggest segment. The construction sector’s value-added grew 9% year-over-year in Q3 2024, with banking system loans for construction up 13.4% during the first eight months of that year. Filipinos are spending on their homes — building new ones, yes, but also fixing, extending, and improving what they’ve got.

Fixed bank loans were designed for buying property in one transaction. They weren’t designed for the way renovation spending actually happens — in stages, across weeks or months, with costs that shift as the project develops. Credit lines fill that gap. They’re not replacing home loans. They’re handling the work that home loans were never built for. And for the homeowner in Quezon City whose bathroom has needed retiling for two years because applying for a full bank loan felt like overkill — that gap closing is overdue.