Home & Decor Blogs: DIY, Interior Design & Lifestyle Ideas

What Happens to Home Equity During Foreclosure

The difference between your home’s market value and the amount you still owe on your mortgage is known as home equity. You have $90,000 in equity if your house is worth $300,000 and you have a loan $210,000. That equity is depleted during foreclosure in a number of ways, including late fees, penalty interest, legal expenses, and the auction discount. Most homeowners leave the process with either nothing at all or a small portion of what they had.

According to ATTOM Data Solutions, the national average foreclosure process takes roughly 592 days from the initial public notice to completion. Before the house ever sells, it is about twenty months’ worth of fees building up against your equity.

How Fees Stack Up Against Your Equity Month by Month

People are surprised by this part because no one takes the time to add everything up until it’s too late.

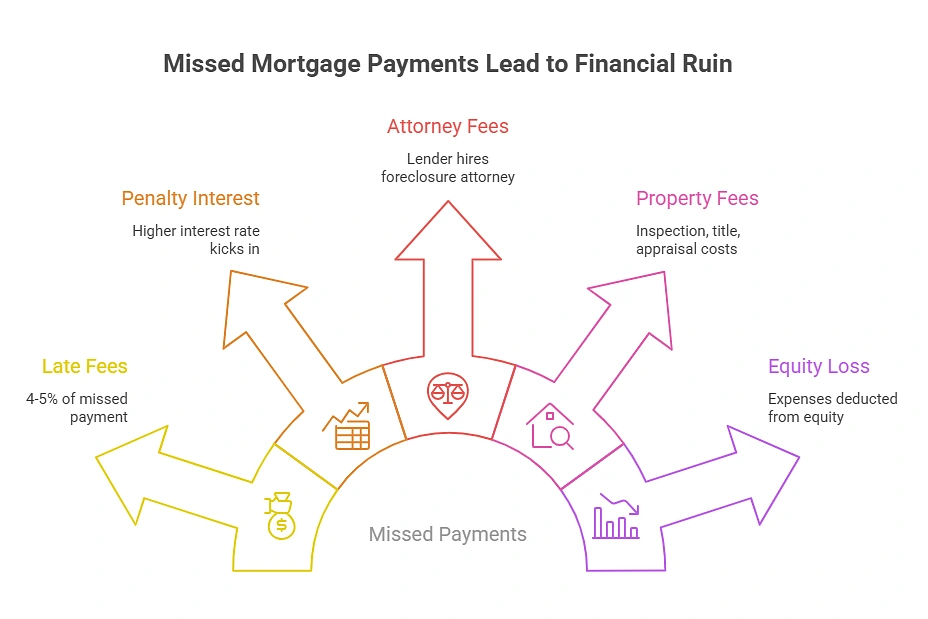

A late fee, usually four to five percent of the monthly payment, is assessed by the lender when you fail to make a payment. That amounts to $56 to $70 for each missed payment on a $1,400 monthly mortgage. It sounds insignificant by itself. However, that is on a monthly basis, and it adds up with everything else.

Here is what accumulates beyond the missed payments themselves:

- Late fees: 4–5% of each missed payment, charged monthly.

- Penalty interest: Some loans have default interest rates that kick in after a certain number of missed payments, sometimes two to five percentage points above the original rate.

- Attorney fees: The lender hires a foreclosure attorney and passes those costs to you. Judicial foreclosures (where the lender has to go through court) run $2,000 to $5,000 or more in legal costs. Non-judicial states are cheaper but still add $1,000 to $2,500.

- Property inspection fees: Lenders send someone to verify the property is occupied and maintained. Each inspection runs $10 to $50 and they might do it monthly.

- Title search and filing fees: $300 to $800 depending on the county.

- Broker price opinions or appraisals: $100 to $400, sometimes multiple times during the process.

Before anybody ever discusses selling the house, the total of those expenses over a 592-day average timeline amounts to $5,000 to $15,000 in expenditures added on top of the actual missing payments, all of which are deducted from your equity.

You have already used up $31,800 of the $90,000 in equity that seemed reasonable a year ago due to fifteen thousand in accumulated fees and twelve months of missed payments at $1,400 each ($16,800), and the house hasn’t sold yet.

The Auction Discount That Takes Most of What Is Left

Foreclosure auctions do not sell homes at market value. They sell them fast, to investors who want a deal and are bidding with cash.

Buyer price demand at foreclosure auction averaged about 55.7 percent of after-repair value according to Auction.com’s marketplace data. This indicates that purchasers are paying about 56% of what the house would be worth if it were properly fixed and listed normally.

The realistic discount for bank-owned houses that are resold after foreclosure ranges from 10 to 30 percent below equivalent market value, depending on holding duration and condition. However, this is only after the bank has taken possession of the property, cleaned it up, and advertised it through standard channels. At the auction itself, discounts run steeper because buyers are taking on risk — no inspections, potential occupants still in the home, unknown repair costs.

What this means for your equity in plain numbers. Say you had $90,000 in equity. Fees and missed payments chewed through $30,000 of it over the foreclosure timeline. Your remaining equity is $60,000 on paper. The home is put up for auction and sold for 25 to 40 percent less than its market worth. That auction price might range from $180,000 to $225,000 for a $300,000 house. At that point, your mortgage balance plus all those accrued fees could reach $250,000 or more. The auction proceeds do not even cover the debt, and your equity is gone entirely.

That is the scenario where the homeowner gets nothing back. It happens more often than the “you might get surplus funds” version that most articles describe.

Junior Liens Take Their Cut Before You See Anything

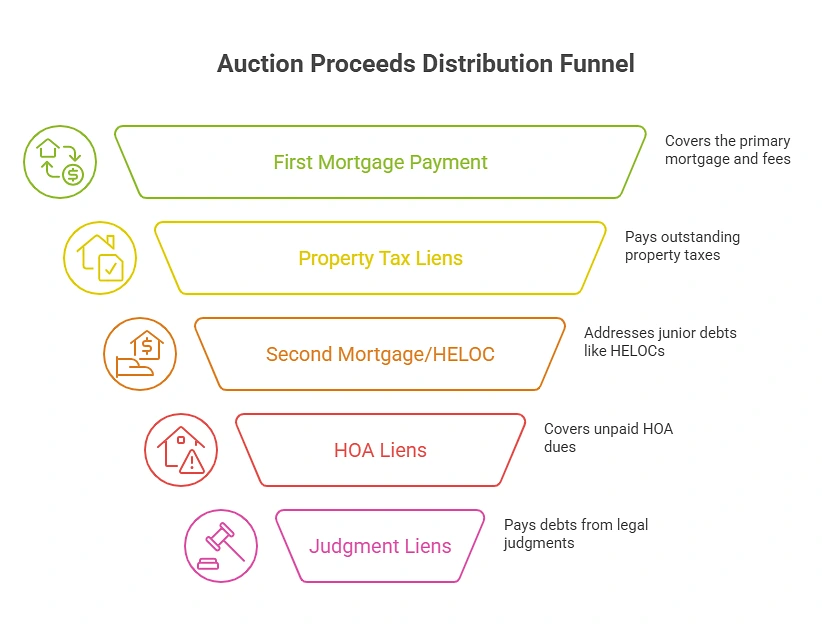

Even in cases where the auction price covers the first mortgage and fees, there is usually a line of other claims waiting.

A junior lien is any debt secured against your property that was recorded after the primary mortgage. Second mortgages, home equity lines of credit, property tax liens, HOA liens, judgment liens from lawsuits — all of these are junior liens and all of them get paid from whatever is left after the first mortgage is satisfied.

The order of payment from auction proceeds works like this:

- First mortgage balance plus all accumulated fees, interest, and legal costs.

- Property tax liens (these sometimes jump ahead of even the first mortgage depending on the state).

- Second mortgage or HELOC balance.

- HOA liens and assessment fees.

- Judgment liens.

- Whatever is left goes to the homeowner.

Most people only think about their first mortgage when they think about equity. But if you took out a $25,000 HELOC three years ago and owe $18,000 on it, and you have a $3,500 property tax lien from last year, and your HOA filed a $2,400 lien for unpaid dues — that is $23,900 in claims you might not have been counting that come out before you see a dollar.

The Timeline Varies Massively by State

Not all foreclosures take 592 days. That is the national average but individual states range from weeks to years, and the length of that timeline directly affects how much equity gets consumed by accumulating costs.

Fast states (non-judicial foreclosure): Texas can complete a foreclosure in as little as 41 days after the notice of default in extreme cases, though recent averages run closer to 135–165 days. Georgia, Virginia, and Alabama also move relatively quickly, often finishing within two to four months. Less time means fewer months of accumulating fees, but it also means less time for the homeowner to act.

Slow states (judicial foreclosure): Louisiana averaged around 3,461 days — over nine years. New York averaged 1,998 days. Hawaii averaged 1,760 days. In these states, the fees and penalty interest accumulate for years. The equity erosion is slower per month but far more total over the full timeline.

Why this matters for your decision: If you are in Texas and you have missed two payments, you might have six to eight weeks before the auction happens. In New York, you might have two years. The window to act — to negotiate a loan modification, arrange a short sale, or sell your house before foreclosure to retain whatever equity remains — is completely different depending on where you live. Knowing your state’s process is not optional; it is the first thing that determines how much time you actually have.

What You Can Do Before the Auction Happens

Once the auction is complete, your options are gone. Everything useful happens before that point.

Loan modification. You request that the lender modify the conditions of your mortgage, such as lowering the interest rate, extending the loan period, or adding the late payments to the loan balance. Before initiating foreclosure, the lender must examine a comprehensive loss mitigation application in accordance with federal servicing regulations. This buys time and occasionally results in payments you can truly afford, but it does not permanently halt the process. The problem is that lenders take a long time to process them, and in some areas, the foreclosure clock continues to run while the application is still waiting.

Short sale. With the lender’s consent, you sell the house for less than what you owe. Even when the selling earnings do not cover the remaining amount, the lender consents to accept them as full settlement of the loan. The lender saves money by not having to complete the foreclosure and sale a REO property, even though you lose the house and the equity. Lenders must approve the sale price for short sales, which can take weeks or months, and not all lenders will do so.

Pre-foreclosure sale at market value. Selling the house on the open market before the foreclosure is finalized allows you to pay down the mortgage, cover the accumulated fees, and keep whatever is left if you still have equity and the time frame permits it. You can only truly leave with money if you take this route. You need a buyer, a close, and a payoff prior to the auction date, which presents a speed problem. Even though the sale price may be slightly less than what a typical listing would bring, pre-foreclosure sellers sometimes wind up dealing with investors or cash buying organizations since cash purchasers close faster than financed buyers. When the auction date is eight weeks away, time typically prevails in the trade-off between price and time.

Deed in lieu of foreclosure. You willingly return the property to the lender. You skip the auction procedure and occasionally bargain for relocation support or a clear release from the outstanding debt, but you lose the house and all equity. This isn’t accepted by all lenders, and some demand that you try to sell first.

The math on foreclosure equity is brutal and it is not complicated. Fees eat into it from day one, the auction discount takes a massive chunk, junior liens take their cut, and what is left — if anything — goes to the homeowner last. The only variable you control is when you act. Every month between the first missed payment and the auction is a month where fees accumulate, options narrow, and the number you walk away with gets smaller. The homeowners who retain equity are almost always the ones who made a decision early, even when the decision was hard.