Home & Decor Blogs: DIY, Interior Design & Lifestyle Ideas

What to Do in the 72 Hours After a Louisiana Storm Damages Your Roof

The first thing to know is that most Louisiana homeowners with visible storm damage should not call their insurance company first. That order matters more than any inspection checklist. Contact your insurer before you understand what your hurricane deductible is, what your damage actually costs to repair, and whether your damage qualifies for a claim under your specific policy language, and you may open a claim that hurts you more than it helps.

Here is the sequence that works, in the actual order Louisiana Department of Insurance guidance from March 2026 walks homeowners through:

- Stabilize the home first. Stop active water intrusion with tarping or emergency dry-in work if the damage is severe.

- Photograph everything before any cleanup. Wide shots and close shots of every damaged area, timestamped, from the roof surface down to interior evidence.

- Check your policy declarations page. Find your hurricane deductible, your named-storm deductible, and any wind or hail exclusions.

- Compare your damage estimate to your deductible. This is the step most homeowners skip and regret.

- Then decide whether to file.

The rest of this article explains why that sequence exists in the current Louisiana insurance environment, and what to inspect for so the claim file you build actually holds up when an adjuster arrives.

Louisiana Deductibles Are the Number That Should Come First

The Louisiana insurance crisis is not over. Insurance Commissioner Tim Temple stated as recently as spring 2026 that the state remains in a property insurance crisis, and while 2025 saw the first rate decreases from a handful of carriers in several years, coverage is still selective and homeowners in coastal parishes are still facing high premiums with high deductibles.

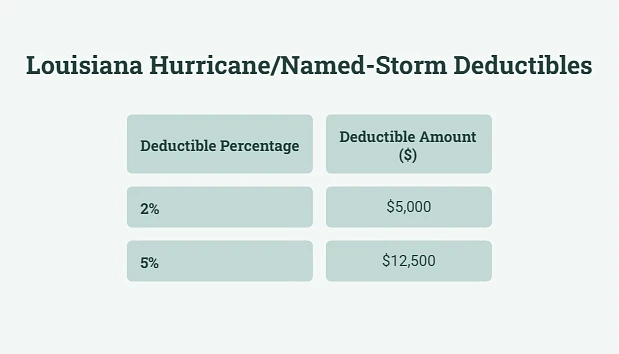

Hurricane and named-storm deductibles in Louisiana typically run 2 to 5 percent of the home’s insured value. Not 2 to 5 percent of the damage. Not 2 to 5 percent of the claim payout. The dwelling coverage amount on your declarations page.

On a home insured for $250,000, that means:

- 2 percent deductible: $5,000 out of pocket before insurance pays anything

- 5 percent deductible: $12,500 out of pocket before insurance pays anything

If a storm causes $8,000 in roof damage and your named-storm deductible is $12,500, filing a claim puts a loss on your record without producing a payout. In the current Louisiana market where carriers are already selective about renewals, that record can affect future coverage.

The homeowner math is straightforward:

- Get a repair estimate from a licensed roofer before calling insurance.

- Compare the estimate to your named-storm deductible.

- If the damage exceeds the deductible enough to make a claim worthwhile after considering the impact on your policy, file. If not, pay out of pocket and keep your record clean.

This is why every serious Louisiana post-storm article should start with the deductible conversation, not with a shingle checklist.

The Difference Between Hail, Wind, and Wind-Driven Rain Damage

Insurance adjusters separate storm damage by cause because policies treat these differently. What you photograph and what you claim depends on which type of damage occurred, and the fingerprints on your roof tell you which one hit you.

Hail damage leaves circular scuffs on shingle surfaces, soft spots where the mat has been bruised beneath the granule layer, cracked ridge caps, and dents in soft metals like vents, gutters, and AC unit fins. Hail damage is usually claimed under general perils coverage, not the higher named-storm deductible.

Wind damage looks different. Look for creased shingles along the exposure line, tabs that have been lifted and no longer seal, exposed nail lines where the shingle above has failed, and missing shingles entirely. Wind damage from a named tropical system falls under your named-storm deductible. Wind damage from a straight-line thunderstorm may fall under general perils. Check your policy.

Wind-driven rain damage shows up inside the house. Ceiling stains that appear days after the storm as water tracks through the roof assembly, damp attic insulation near the ridge or over exterior walls, drip trails along valleys or at wall intersections, musty odors in closets that back to exterior walls. Wind-driven rain is often the actual cause of interior damage in Louisiana storms, and the delayed timing (interior stains appearing days after the exterior damage occurred) is why the LDI guidance emphasizes photographing the roof before cleanup even if you don’t yet see interior evidence.

Documenting all three types matters because insurance adjusters use the presence or absence of specific fingerprints to determine what caused what. A roof with hail bruising and no interior stains gets a different scope than a roof with wind creasing and delayed ceiling stains.

What to Inspect From the Ground Before Anyone Climbs the Roof

Most of the inspection you can do safely happens from ground level or from an interior attic check. This is what belongs in your photo file before you contact anyone.

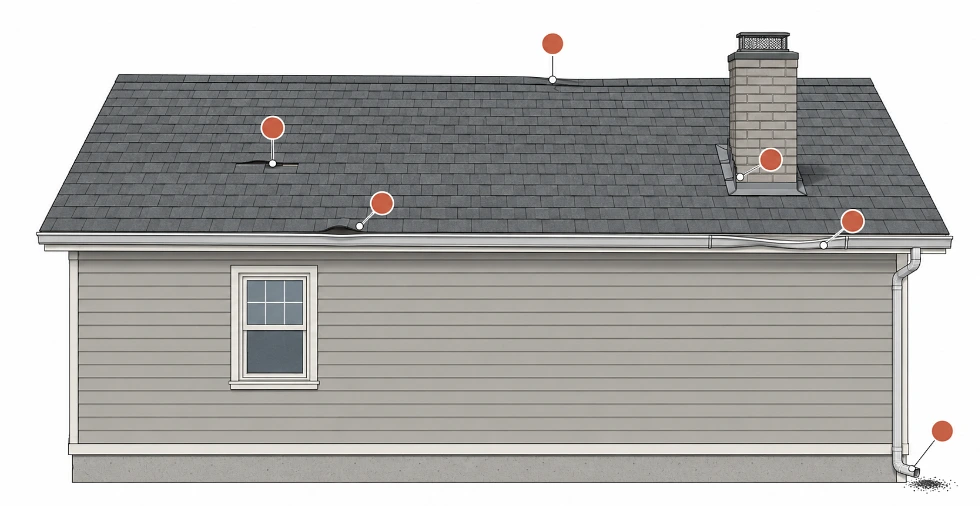

From the ground, walking the perimeter of the house:

- Missing shingles anywhere on the visible roof planes. Note quantity and location.

- Lifted shingle edges that break the horizontal line of the roof. These are wind damage even if the shingle is still attached.

- Debris on the roof surface. Branches, projectile damage, anything that impacted the roof needs a close-up photo.

- Damaged or bent flashing around chimneys, vent stacks, and skylights, visible from below.

- Gutter damage. Dents in the front face of the gutter (usually hail), separation from the fascia (usually wind), or granules pooled at downspout discharge points (indicates shingle mat exposure).

- Sagging roof sections or a warped roofline visible from a distance. Step back into the yard and look at the ridge line. It should be straight.

From inside the attic within 24 hours of the storm, safety permitting:

- Damp insulation in any area, especially near the ridge, over exterior walls, or around penetrations.

- Water stains on the underside of the roof deck. Dark spots on the sheathing where water has soaked through.

- Daylight visible through the roof structure. Any hole you can see through is an obvious priority.

- Wet rafters or sheathing even if the surface below appears dry. Moisture wicks along wood before it drips.

Everything above can be photographed by the homeowner. What comes next requires a licensed roofer.

What Only a Professional Can Safely Assess

The damage most homeowners can’t see from the ground is where insurance claims are actually won or lost. Getting a licensed roofer in Louisiana on the roof for a documented inspection before your adjuster arrives changes the dynamic of the entire claim. The roofer documents damage the adjuster might miss, provides manufacturer and material documentation, and produces a scope of work that the adjuster’s initial estimate can be compared against.

Specifically, a professional inspection captures:

- Flashing condition at chimneys, valleys, and wall transitions. This is where wind-driven rain enters even when the field shingles look intact.

- Fastener exposure. Nail heads visible through the shingle surface, or nails that have backed out from wind uplift cycling.

- Shingle mat bruising that isn’t visible from below. Soft spots that indicate hail impact without visible granule loss.

- Underlayment condition where shingles have lifted. If the underlayment has failed, water has already reached the deck.

- Ridge and hip damage. These are the highest-elevation, most-exposed points of the roof and typically show damage first.

- Attic penetration inspection. Skylights, plumbing vents, and roof-to-wall transitions.

The inspection report becomes part of the claim file. In Louisiana’s current insurance environment, where adjusters are handling high claim volumes and initial scopes often need supplements to reflect the actual damage, having your own roofer’s documented assessment before the adjuster arrives is worth significantly more than a general homeowner description of “there’s some missing shingles.”

The FORTIFIED Question

Louisiana homeowners repairing or replacing storm-damaged roofs increasingly ask about the FORTIFIED program because it offers real insurance discounts.

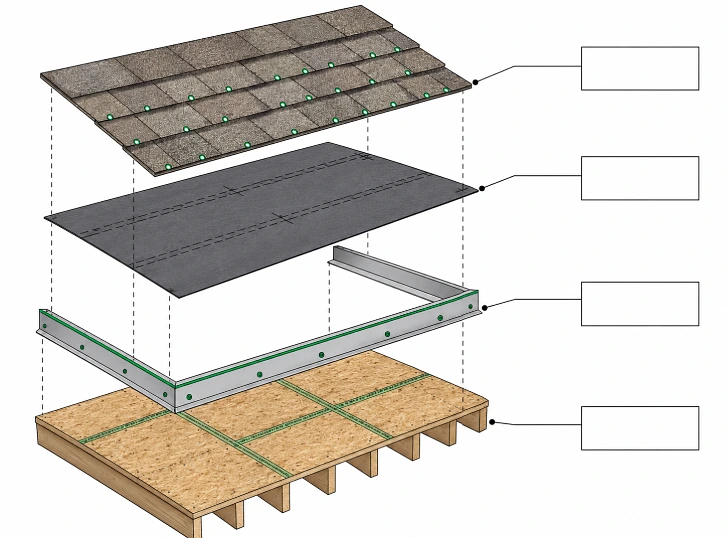

FORTIFIED Roof is a designation from the Insurance Institute for Business and Home Safety (IBHS) that certifies the roof was installed to hurricane-resistance standards, including sealed roof deck, reinforced edges, upgraded fasteners, and specific installation methods that resist wind uplift and wind-driven rain.

For Louisiana homeowners, the practical implications:

- Insurance discounts for FORTIFIED Roof certification vary by carrier but typically range from 7 to 35 percent off the wind portion of the premium.

- Louisiana Fortify Homes Program grants provide up to $10,000 toward the cost of upgrading to a FORTIFIED Roof during a qualifying reroof.

- The upgrade during repair is often the smart moment to do this. If the roof needs replacement anyway due to storm damage, the incremental cost to upgrade to FORTIFIED specifications during that replacement is meaningfully less than doing it as a standalone project later.

Ask any roofer providing a replacement estimate whether their scope is FORTIFIED-eligible and whether they’re registered as a FORTIFIED-designated contractor. Not every roofer holds this certification, and the ones who do can walk a homeowner through the grant application and the insurance discount process.

Contractor Screening After a Louisiana Storm

The current LDI guidance also warns about contractors who show up after storm events with door-to-door pitches, urgency framing, and requests for upfront payment or claim assignment.

Legitimate Louisiana roofers verify as follows:

- Louisiana State Licensing Board for Contractors (LSLBC) registration, verifiable through the state licensing database.

- Physical business address in Louisiana, not a truck and a phone number.

- Proof of general liability insurance and workers compensation coverage that you can request to see.

- References from Louisiana homeowners in your parish or a nearby parish with completed work more than a year old, so you can verify durability.

- A written scope of work that specifies materials, tear-off, underlayment, flashing replacement policy, and warranty terms before any signed contract.

Warning signs that should end the conversation immediately: any request for full payment upfront, any pressure to sign a contract on the spot, any request that you assign your insurance benefits to the contractor (a legitimate roofer bills the homeowner, not the insurance company), any claim that they can “get your insurance to pay for a new roof” when the damage doesn’t warrant it.

The 72-Hour Timeline

Everything above compresses into a specific timeline the LDI guidance and Louisiana roofers converge on:

- Hours 0 to 6 after the storm ends: Safety first. Downed lines, unstable trees, structural hazards. Do not go on the roof. Do not enter parts of the house with active water intrusion or ceiling sagging.

- Hours 6 to 24: Ground-level and interior photo documentation. Attic check. Emergency dry-in if there is active water intrusion (tarping, temporary patches). Save receipts.

- Hours 24 to 48: Contact a licensed Louisiana roofer for a documented inspection. Review your insurance policy declarations page. Calculate the damage estimate against your named-storm deductible.

- Hours 48 to 72: If the damage justifies filing, open the claim with a complete photo file and the roofer’s inspection report ready to submit. If it doesn’t, schedule the repair directly with your roofer and skip the claim.

The homeowners who follow this sequence end up with either a clean claim that gets paid without a fight, or a repair they paid for out of pocket without putting an unnecessary loss on their insurance record. The homeowners who skip the sequence and call insurance first often end up with a claim opened before they understood what it would actually cost them, and no way to close it once it’s on the file.

Louisiana’s climate makes storm damage inevitable. The insurance environment is what makes the response strategy matter. Get the sequence right and both problems become manageable. Get it wrong and the storm ends up being the cheaper of the two problems you’re now dealing with.